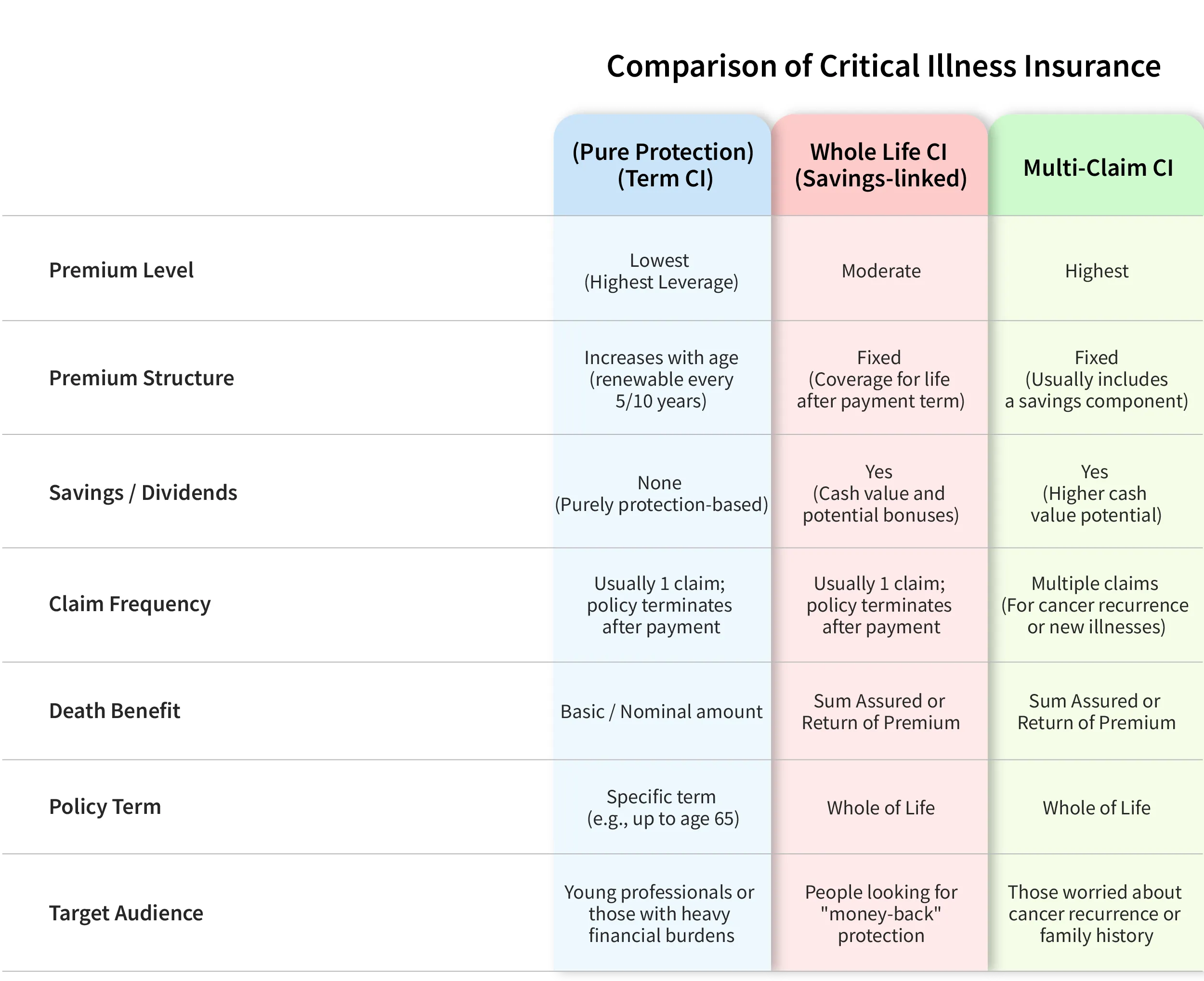

Critical Illness Insurance

Critical illness insurance aims to provide financial protection for policyholders diagnosed with specific major diseases. When the insured is first diagnosed with any covered severe illness, such as cancer, heart attack, or stroke, the insurance company pays a substantial lump sum. This payout is unrestricted, allowing the insured to use the funds for medical expenses, rehabilitation costs, or other living expenses as needed. This type of insurance helps alleviate the financial burden during challenging health situations, ensuring access to necessary care and support.

Critical Illness Insurance

When the insured is diagnosed with a major illness, Critical Illness (CI) insurance provides a lump-sum payment.

This payment helps cover high medical costs or other related expenses, significantly reducing financial pressure on the patient and family. The funds can also replace lost income, allowing the insured to focus fully on recovery.

Flexible Use

The lump-sum payout from Critical Illness (CI) insurance can be used for any need, offering high flexibility.

Uses include covering medical expenses, rehabilitation treatments, daily living expenses, or providing general family support. This allows policyholders to freely utilize the funds based on their specific situation, alleviating overall financial strain.

Additional Coverage

Many Critical Illness (CI) insurance plans offer valuable additional coverage beyond the core benefit, significantly boosting policyholders' security.

These enhancements often include coverage for accidental death or disability benefits. By integrating these extra protections, the policies provide a more comprehensive safety net, further enhancing the policyholder's and their family's sense of financial security.

Learn more

Frequently Asked Questions

The payout amount for critical illness insurance is usually based on the amount chosen at the time of purchase and is paid in full upon diagnosis.

How is the premium for critical illness insurance calculated?

How do I file a claim for critical illness insurance?

Who is this type of insurance suitable for?

How should I choose the right critical illness insurance?

What are the risks associated with critical illness insurance?

Blog

危疾定義立標準 減少理賠爭議性

......有感體力大不如前,想在目前健康狀態下,投保危疾產品,但坊間品牌選擇眾多,加上同類產品條款不一,難以用性價比去衡量,......

懷孕十八周 胎兒可投保

新婚一年後打算增添家庭成員,由於自己是「高齡產婦」,故來信詢問如何為未來寶寶規劃保障。

未出生嬰兒 可購危疾保

聽說未出生的嬰兒也可以購買危疾保險,想為嬰兒作準備。故來信希望了解為未出生的嬰兒選擇危疾保險時應注意哪些事項?

選購危疾保 查看家族病

市面上保險產品花多眼亂,不同保險公司的顧問,每位都「賣花讚花香」,究竟在選擇時有甚麼需要注意呢?

儲蓄危疾保 長供勝短供

......想配置危疾,給自己及家人一個保障。危疾供款時間比較長,本人擔心萬一生意差,供不起保單,會浪費多年的供款。本人身體一些位置有結節問題,雖然情況穩定,但很多保險中介都說有不保的可能性,對於本人這種情況和顧慮,應該如何解決。

Blog

危疾定義立標準 減少理賠爭議性

......有感體力大不如前,想在目前健康狀態下,投保危疾產品,但坊間品牌選擇眾多,加上同類產品條款不一,難以用性價比去衡量,......

懷孕十八周 胎兒可投保

新婚一年後打算增添家庭成員,由於自己是「高齡產婦」,故來信詢問如何為未來寶寶規劃保障。

未出生嬰兒 可購危疾保

聽說未出生的嬰兒也可以購買危疾保險,想為嬰兒作準備。故來信希望了解為未出生的嬰兒選擇危疾保險時應注意哪些事項?

Load More

Difference between Broker & Agency

- BrokerAgency

- Comparing various products from multiple insurance companies all at once.

- Exaggerate the company's customized policies and reduce premium costs.

- From tailor-made analysis to chasing claims, protecting customer interests first

- Take advantage of the company's limited-time offers to secure high-value policies.

- Proactively reviewing your policy and dynamically adjusting life coverage.

Contact Us

How much do I need for retired?

We help you figure it out.

CALCULATE NOW